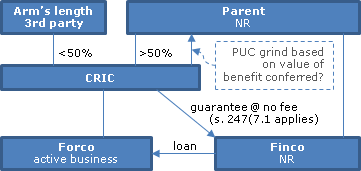

Q.1 (Application of the Foreign Affiliate Dumping Rules to CRIC Guarantees)

Assume that CRIC is majority (but not wholly) owned and controlled by...

The text of this content is paywalled except for the first five days of each month. Subscribe or log in for unrestricted access.

{kind=link}