Subsection 247(1)

Transaction

See Also

Cameco Corporation v. The Queen, 2018 TCC 195, aff'd 2020 FCA 112

As part of a preliminary discussion of s. 247(2), Owen J stated (at para. 677):

An “arrangement” includes an informal agreement or a plan,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | having a Swiss/Lux subsidiary enter into long-term purchase contracts at a somewhat fixed price with third parties and the taxpayer did not engage s. 247(2) | 708 |

| Tax Topics - General Concepts - Sham | transactions that were not factually misrepresented were not a sham | 254 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | "series" concept narrowly interpreted to permit comparison with arm's length transactions | 82 |

Subsection 247(1.3)

Finance

“Consultation on Reforming and Modernizing Canada's Transfer Pricing Rules” 6 June 2023

- The profit allocations that were accepted in Cameco were reached based on relationships created by intra-group contractual arrangements,...

Subsection 247(2)

Cases

AgraCity Ltd v. Canada, 2016 DTC 5006 [at 6525], 2015 FCA 288

The taxpayer (“AgraCity”) was wholly-owned by Jason Mann. A Barbados corporation ("NewAgco-Barbados") was wholly-owned by a second...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Federal - Tax Court of Canada Rules (General Procedure) - Section 53 | inconsistent assessments of related taxpayers | 240 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1) | inconsistent assessments of related taxpayers | 180 |

| Tax Topics - Other Legislation/Constitution - Federal - Tax Court of Canada Rules (General Procedure) - Section 82 | inconsistent assessments of related taxpayers | 307 |

Canada v. GlaxoSmithKline Inc., 2012 DTC 5147 [at at 7338], 2012 SCC 52, [2012] 3 S.C.R. 3

The taxpayer purchased an active pharmaceutical ingredient from an affiliated non-resident corporation ("Adechsa") for approximately five times...

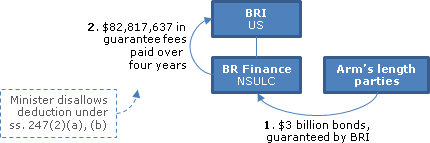

Canada v. General Electric Capital Canada Inc., 2011 DTC 5011 [at at 5558], 2010 FCA 344

The Minister disallowed the deduction by the taxpayer of guarantee fees paid by it to its US parent. The fees were calculated as 1% of the face...

See Also

Singapore Telecom Australia Investments Pty Ltd v Commissioner of Taxation, [2024] FCAFC 29

The taxpayer (“STAI”) - a wholly-owned Australian subsidiary of a Singapore public company - purchased in June 2002 all the shares of an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 9 | an independent enterprise would have agreed to allow interest to be capitalized, but not to make it contingent on cash flow | 657 |

Cameco Corporation v. The Queen, 2018 TCC 195, aff'd 2020 FCA 112

The taxpayer’s newly-incorporated subsidiary (“CESA,” which was a two-employee Swiss branch of a Luxembourg company and was later succeeded...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Sham | transactions that were not factually misrepresented were not a sham | 254 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(10) | "series" concept narrowly interpreted to permit comparison with arm's length transactions | 82 |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(1) - Transaction | meaning of "arrangement" and "event" | 153 |

Alberta v ENMAX Energy Corporation, 2018 ABCA 147

A wholly-owned subsidiary (ENMAX) of the City of Calgary made 10-year subordinated term loans to ENMAX power-distribution subsidiaries at interest...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) - Subparagraph 20(1)(c)(i) | interest on a loan from a tax-exempt parent should be at an arm’s length rate reflecting implicit parental credit support | 494 |

| Tax Topics - General Concepts - Tax Avoidance | right to structure affairs to reduce taxes (or, here, payments in lieu) inapplicable where consumer assistance purpose defeated | 189 |

| Tax Topics - Statutory Interpretation - Hansard, explanatory notes, etc. | purpose inferred in part from Legislative Assembly statement of Minister | 83 |

| Tax Topics - Income Tax Act - Section 67 | test of whether the amount was objectively reasonable | 293 |

Chevron Australia Holdings Pty Ltd v Commissioner of Taxation, [2017] FCAFC 62

The U.S. subsidiary (“CFC”) of the taxpayer (“CAHPL” – which was an Australian subsidiary in the Chevron multinational group) borrowed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 9 | cross-border loan interest improperly reflected lack of security | 387 |

| Tax Topics - Statutory Interpretation - Retroactivity/Retrospectivity | retroactive tax was constitutional if it could be judicially challenged based on the facts | 476 |

Sifto Canada Corp. v. The Queen, 2017 TCC 37

CRA accepted a voluntary disclosure by Sifto Canada that it had undercharged on its sales of rock salt to a U.S. affiliate, and reassessed...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 9 | agreement with the U.S. competent authority re a VDP-adjusted transfer price binds CRA even if it had not yet audited the taxpayer | 593 |

| Tax Topics - Income Tax Act - Section 115.1 - Subsection 115.1(1) | 115.1 not germane to subsequent inconsistent CRA assessment | 201 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1) | MAP agreement concurred in by taxpayer was binding on the Minister as it was not “indefensible” | 265 |

Suncor Energy Inc. v. The Queen, 2014-4179(IT)G

Petro-Canada U.K. Limited (“PCUK”), which carried on its energy business in the U.K., was wholly owned by Holdings UK, which was wholly-owned...

ENMAX Energy Corp. v. Alberta, 2016 ABQB 334, rev'd 2018 ABCA 147

An Alberta utility (EEC) was required to make payments to the province equal to the provincial and federal income tax to which it would have been...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 20 - Subsection 20(1) - Paragraph 20(1)(c) | 11.5% interest rate on unsecured intercompany note was reasonable under s. 20(1)(c) notwithstanding that this exceeded an arm’s length rate of around 8.5% | 513 |

| Tax Topics - Income Tax Act - Section 67 | Gabco test implies a range | 122 |

Re Nortel Networks Corp., 2014 ONSC 6973

Under Nortel's transfer pricing methodology, the entities performing R&D, including Nortel itself and a UK subsidiary, were entitled to all...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 9 | provision, under multinational agreement for residual profit split method, for unilateral bearing of restructuring costs, represented appropriate ex ante risk allocation | 469 |

AgraCity Ltd. v. The Queen, docket 2014-1537

In her Reply, the Minister alleged that a Barbados corporation ("NewAgco") which did not deal at arm's length with the taxpayer, took over a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 163 - Subsection 163(2) | Reply must explain specific bases on which a penalty was imposed | 268 |

| Tax Topics - Other Legislation/Constitution - Federal - Tax Court of Canada Rules (General Procedure) - Section 53 | argument inconsistent with assumed facts struck from pleadings, but might be reintroduced at trial as an alternative argument | 172 |

McKesson Canada Corporation v. The Queen, 2014 DTC 1197 [at at 3749], 2014 TCC 266

Boyle J, after finding in McKesson that the taxpayer had been selling its trade receivable to its immediate Luxembourg parent (MIH) at discounts...

Marzen Artistic Aluminum Ltd. v. The Queen, 2014 DTC 1145 [at at 3433], 2014 TCC 194, aff'd 2016 DTC 5018 [at 6600], 2016 FCA 34

{kind=link}

In 2000 and 2001 the Canadian-resident taxpayer, which manufactured windows in British Columbia, paid Cdn.$4.2M and Cdn.$7.8M in fees under a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(4) | no explanation of derivation of pricing | 111 |

McKesson Canada Corporation v. The Queen, 2014 DTC 1040 [at at 2723], 2013 TCC 404

With "the predominant purpose...of...the reduction of its Canadian tax on its profits" (para. 18), the taxpayer, which was an indirect Canadian...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | expert reports without testimony | 56 |

| Tax Topics - General Concepts - Purpose/Intention | tax purpose v. commercial result | 92 |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(4) | advocacy 3rd-party report not read by taxpayer | 163 |

| Tax Topics - Treaties - Income Tax Conventions - Article 9 | 5-year limitation did not apply to secondary Part XIII assessment | 206 |

Burlington Resources Finance Company v. The Queen, 2013 DTC 1190, 2013 TCC 231

{kind=link}

This decision concerned motions to amend or strike pleadings.

The taxpayer, a Nova Scotia unlimited liability company, raised U.S.$3 billion in...

Alberta Printed Circuits Ltd. v. The Queen, 2011 DTC 1177 [at at 967], 2011 TCC 232

The Canadian taxpayer was in the business of printing custom electronic circuits. Pizzitelli J. found that the taxpayer was not dealing at arm's...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 251 - Subsection 251(1) - Paragraph 251(1)(c) | common interests and implementation | 352 |

| Tax Topics - Treaties - Income Tax Conventions - Article 26 | 96 | |

| Tax Topics - Treaties - Income Tax Conventions - Article 9 | 96 |

Ford Motor Co. of Canada, Ltd. v. Ontario Municipal Employees Retirement Board, 2004 DTC 6224 (Ont. Sup. Ct. of J.)

In the context of a determination of what was the fair value of shares held by minority shareholders of a Canadian auto subsidiary ("Ford Canada")...

Safety Boss Ltd. v. The Queen, 2000 DTC 1767 (TCC)

Because of the reputation and the prior personal contacts of the taxpayer's shareholder ("Miller") with officials of the Kuwait Oil Company, in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | conferral on corp increasing its value is benefit conferred on shareholder | 149 |

| Tax Topics - Statutory Interpretation - Interpretation Bulletins, etc. | 53 |

Administrative Policy

27 February 2024 CTF Transfer Pricing Roundtable

“Delineation” of a transaction

Consistent with the transfer-pricing guidelines (TPG), the delineation process requires outlining what has...

7 July 2022 Internal T.I. 2021-0893791I7 - Interest expense on subordinated income instrument

Holdco, a subsidiary of a U.S. entity (“Parent”), provided long-term debt financing to its Canadian operating entities (“Opcos”) in the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 9 | OECD principles re interest on related-party debt | 210 |

17 May 2023 IFA Roundtable Q. 1, 2023-0964391C6 - stock based compensation and transfer pricing

Does CRA expect Canadian taxpayers to include stock option expenses in the cost of services charged to related non-residents, where the employees...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 7 - Subsection 7(3) - Paragraph 7(3)(b) | s. 7(3)(b) non-deduction or s. 112(1)(e) deductibility could apply to cross-border stock option recharges of non-resident parent | 167 |

27 October 2020 CTF Roundtable Q. 12, 2020-0862501C6 - COVID-19 and Prior APAs/Current MAPs

What is the COVID-19 impact on: previously negotiated advance pricing arrangements (“APAs”); mutual agreement procedures (“MAPs”) that are...

28 May 2019 Internal T.I. 2018-0772971I7 - Interaction between sections 94, 17, 247

The beneficiaries of CdnTrust, a trust resident in Canada that wholly-owns Canco, and of NRTrust, a factually non-resident trust that wholly-owns...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 94 - Subsection 94(2) - Paragraph 94(2)(f) | failure to charge for services rendered by a Canco to a NR sub of a NR trust tainted the NR trust under s. 94(2) | 258 |

| Tax Topics - Income Tax Act - Section 94 - Subsection 94(2) - Paragraph 94(2)(a) | NIB loan by a Canco to a NR sub of a NR trust tainted the NR trust under s. 94(2) | 222 |

| Tax Topics - Income Tax Act - Section 17 - Subsection 17(1) | triggering of s. 94(2)(a) by interest-free loan to the sub of a non-resident trust was independent of the application of s. 17 to the loan | 262 |

26 February 2019 Toronto CRA & Tax Professionals Seminar

CRA comments relating to the mooted BEPS impact on CRA transfer-pricing practices included:

- BEPS Actions 8 to 10 did not effect substantial...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(4) - Paragraph 247(4)(a) | penalties typically imposed where missing or unsubstantiated analysis | 107 |

13 December 2018 Wheaton Precious Metals Press Release

Wheaton Precious Metals (“Wheaton”) through its Caymans subsidiaries, earns income on precious metal streaming contracts, i.e., precious metal...

2018 Ruling 2017-0729431R3 - Transfer Pricing Adjustment and Earnings

CRA assessed a Canadian subsidiary (Canco 1) in a Canadian multinational group under s. 247(2) on the basis that the fees earned by a sister...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) - Paragraph 5907(2)(f) | fictional transfer pricing adjustments did not affect the exempt surplus calculation (other than for the foreign taxes adjustment) | 579 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Net Earnings - Paragraph (a) | MAP downward adjustment to foreign income taxes increased net earnings | 253 |

27 November 2018 CTF Roundtable Q. 4, 2018-0779931C6 - OECD TP Guidelines

Will the 2017 OECD Transfer Pricing Guidelines be applied retroactively on the basis that they are just clarifying the previous versions of the...

Alexandra MacLean, "CRA Audits of Large Corporations - The view from ILBD" under Responses to recent adverse decisions – Cameco, 27 November 27 2018 CTF Annual Conference.

Cameco, which is under appeal, has not affected the CRA operation of its transfer pricing audit program (business as usual).

27 October 2017 Internal T.I. 2017-0694231I7 - Subsection 247(2), surplus, and FAPI

Where, as a result of an s. 247(2) transfer pricing adjustment respecting a transaction between Canco and CFA for the sale of goods or provision...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 53 - Subsection 53(1) - Paragraph 53(1)(c) | sale of goods at undervalue to sub does not imply a contribution of capital | 180 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(2) | effect on surplus balances of foreign transfer-pricing adjustment might be reversed under Reg. 5907(2) | 157 |

| Tax Topics - Income Tax Regulations - Regulation 5907 - Subsection 5907(1) - Earnings - Paragraph (a) | surplus could be adjusted by transfer-pricing adjustment | 140 |

26 April 2017 IFA Roundtable Q. 2, 2017-0691191C6 - Subsection 247(2) and FAPI

Does s. 247 apply in computing a foreign affiliate’s foreign accrual property income in the context of a transaction between it and another...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(f) | s. 247(2) applies for FAPI purposes | 115 |

RC4651 “Guidance on Country-By-Country Reporting in Canada” 23 November 2018

CbCR data not used directly in assessing

Appropriate use of CbCR reporting information

The BEPS Action 13 Final Report sets out three permitted...

14 September 2016 Internal T.I. 2016-0631631I7 - Transfer pricing capital adjustment

In Year X , Canco buys a non-depreciable capital property from its non-resident parent (Forco) for $10,000,000, sells the property for $15,000,000...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(3) | no statute-barring applies to initial assessments of transfer-pricing penalties | 326 |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(11) | s. 152(4) limits apply to additional s. 247(3) assessments | 161 |

16 November 2016 Toronto Centre Canada Revenue Agency & Tax Professionals Seminar on International Tax Issues

Points included:

- BEPS Actions 8 to 10 (re transfer pricing) were examined and determined to not require any changes to the s. 247 rules, and the...

2015 Ruling 2014-0542411R3 - Carrying on business in Canada and PE

Various ForCo employees are key to large construction “Projects” of its Canadian sister. They will be “seconded” to the ForCo, so that...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 5 | PE in Canada of ForCo avoided through seconding employees to its Cdn sister and meeting in Canada up to 90 days annually only offsite | 533 |

| Tax Topics - Income Tax Regulations - Regulation 102 - Subsection 102(1) | payroll reimbursement payments under employee secondment arrangement not subject to Reg. 105 | 219 |

| Tax Topics - Income Tax Act - Section 5 - Subsection 5(1) | seconded employees respected as employees notwithstanding their payroll is paid by (and reimbursed to) ForCo | 59 |

TPM-17 “The Impact of Government Assistance on Transfer Pricing” 2 March 2016

4. When a cost-based transfer pricing methodology is used to determine the transfer price of goods, services, or intangibles sold by a Canadian...

23 February 2016 Toronto Centre Tax Professionals Seminar under “Perception that BEPS is Being Applied”

In response to a question respecting a “perception that BEPS is already in the process of being applied by auditors,” CRA stated...

1 September 2015 Internal T.I. 2013-0507381I7 - Transfer pricing adjustments and gross revenue

CRA considered that an upward adjustment to a Canadian resident’s sales proceeds – but not a downward adjustment to its purchase price for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Regulations - Regulation 402 - Subsection 402(3) | s. 247(2) increases to proceeds (but not downward adjustments to purchase prices) increase gross revenue for provincial allocation purposes | 233 |

| Tax Topics - Income Tax Act - Section 248 - Subsection 248(1) - Gross Revenue | sales (but not purchases) transfer pricing adjustments to gross revenue | 45 |

TPM-16 "Role of Multiple Year Data in Transfer Pricing Analyses" 29 January 29 2015

Selecting the most appropriate point in the range

28. When several comparable transactions or results are acceptable, an arm's length range will...

TPM-15 "Intra-group services and section 247 of the Income Tax Act" 29 January 2015

Direct v. indirect charges

10. … The direct charge method attaches a specific charge to each identifiable service. The indirect charge method...

3 October 2014 Internal T.I. 2014-0532051I7 - Rent and Part XIII Tax

A non-resident individual not carrying on business in Canada leases a Canadian property to a related resident individual at less than fair market...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(1) - Paragraph 212(1)(d) | non-commercial arrangement not subject to s. 247 but is subject to Part XIII/property taxes included in rent/no Part XII tax on imputed rent | 247 |

| Tax Topics - Income Tax Act - Section 3 - Paragraph 3(a) - Business Source/Reasonable Expectation of Profit | rents from personal rental property not required to be reported | 112 |

10 October 2014 APFF Roundtable Q. 26, 2014-0538201C6 F - 2014 APFF Roundtable, Q. 26 - Cost of property

On a non-arm's length transfer of capital property by a non-resident in favour of a resident Canadian, whether by donation or disposition, what...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | definition of FMV, which may differ from the s. 247 arm's length price | 182 |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(3) - Paragraph 247(3)(a) - Subparagraph 247(3)(a)(iii) | general requirement for penalty elimination re transfer pricing capital setoff adjustment | 146 |

15 November 2013 Internal T.I. 2013-0478621I7 F - Transfer of intangibles - TP adjustments

Pursuant to a sales agreement between Canco, its immediate non-resident parent (Parent) and the ultimate U.S. parent of Canco (Pubco), as vendors,...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 56 - Subsection 56(2) | secondary adjustment re group sale with Canco not charging for intangibles | 248 |

| Tax Topics - Income Tax Act - Section 69 - Subsection 69(4) | s. 69(4) inapplicable where grandchild Canco undercharges for asset sale, enhancing sales proceeds received by ultimate U.S. parent | 176 |

31 October 2012 TPM-14 "2010 Update of the OECD Transfer Pricing Guidelines"

After noting that in the 2010 version of the OECD Transfer Pricing Guidelines "there is no strict hierarchy to be applied to the selection of a...

5 October 2012 Roundtable, 2012-0454201C6 F - Nouvelle Circulaire - Prix transfert international

Does the CRA intend to issue a new version of IC87-2R that will reflect the new 2010 version of the OECD Guidelines? CRA responded:

The CRA does...

5 October 2012 Roundtable, 2012-0451241C6 F - Benefit conferred on a NR shareholder by a NR corp

After finding that the gratuitous use by the non-resident shareholder of a Canadian property of the non-resident corporation likely produced a s....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(3) - Paragraph 214(3)(a) | gratuitous use by NR shareholder of Canadian property of the NR corporation produces a s. 214(3)(a) deemed dividend | 158 |

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(7) | s. 15(7) assists in determining that s. 15 can apply to the NR shareholder of a NR corporation gratuitously using the corporation’s Canadian property | 73 |

5 October 2012 Roundtable, 2012-0454221C6 F - Allocation des risques et contrôle

Canco entered into an exclusive supply agreement with an arm’s length US customer which required it to establish a plant in the U.S. close to...

6 December 2011 Roundtable, 2011-0427301C6 - 2011 TEI-CRA Liaison Meeting: Qu.11

As many treaties have limitation periods for making assessments, CRA considers it inadvisable to delay making a Part XII tax assessment arising...

6 December 2011 TEI-CRA Liason Meeting Roundtable Q. 6, 2011-0427261C6 - 2011 TEI-CRA Liaison Meeting: Qu. 6

As part of a discussion of the advance pricing agreement program, CRA stated:

We have determined that business restructuring cases are not...

6 December 2011 TEI-CRA Liason Meeting Roundtable Q. 10, 2011-0427291C6 - 2011 TEI-CRA Liaison Meeting: Qu. 10

As part of a response to a query that noted that CRA auditors often raise potential transfer pricing adjustments simply because it is easy to do...

6 December 2011 TEI-CRA Liason Meeting Roundtable Q. 12, 2011-0427311C6 - 2011 TEI-CRA Liaison Meeting: Qu.12

After noting that (in comparison to the 1995 version) the 2010 version of the OECD Transfer Pricing Guidelines did not so much de-emphasize the...

Transfer Pricing Memorandum TPM-06, “Bundled Transactions” 16 May 2005

Even though there is no explicit reference to a bundled transaction or a requirement to separately price property or services in the Act (other...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 12 | distinction between know-how and services provision | 215 |

2 December 1999 Internal T.I. 1999-0010070 - Guarantee fee

Where a Canadian parent corporation and its U.S. subsidiary participate in a shared credit facility and each guarantees the loan made to the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 64 |

Articles

Franco-Nevada Press Release, "Franco-Nevada Reaches Settlement on Canadian Tax Disputes", 11 September 2025 Press Release of Franco-Nevada Corporation

Franco-Nevada Corporation ("Franco-Nevada") announced the settlement with CRA of its appeal of reassessments under the transfer pricing rules for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(1) - Investment Business | CRA agreed in settlement that precious metal streaming agreements did not give rise to FAPI | 157 |

Christopher J. Montes, Siobhan A.M. Goguen, "Recharacterization of Transactions Under Section 247: Still an Exceptional Approach", 2018 Conference Report (Canadian Tax Foundation), 21:1-25

“Accurate delineation” approach in 2017 OECD Guidelines is in fact an economic substance approach (pp. 21:11-12)

The 2017 guidelines allow a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 9 | 2017 OECD transfer-pricing guidelines mandate an “accurate-delineation approach” that is contrary to s. 247(2) | 276 |

Byron Beswick, "Transfer Pricing and Transactions Between Foreign Entities", Canadian Tax Journal, (2019) 67:1, 187-208

Overview (p. 188)

[A] textual, contextual, and purposive analysis of section 247 and other Canadian transfer-pricing provisions, in particular...

Adrian Tan, "The Emergence of the Profit-Split Method", Canadian Tax Highlights, Vol. 27, No. 2, February 2019, p. 1

Where profit-split method (PSM) is appropriate in transfer pricing (TP) (p. 1)

The PSM is considered to be the most appropriate method if (1) both...

Matias Milet, Jennifer Horton, "The Canada Revenue Agency’s Interpretation of the 2017 OECD Transfer Pricing Guidelines", International Tax (Wolters Kluwer CCH), No. 103, December 2018, p.10

CRA intent to apply the 2017 Transfer Pricing Guidelines to pre-2017 taxation years (pp. 10-11)

The CRA indicated [in 2018 CTF Rouundtable, Q.4]...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 9 | 306 |

Nathan Boidman, "Cameco and Cash-Boxes", 19 December 10 2018

OECD cash box notion

[T]he Cameco case…effectively rejected the OECD/base erosion and profit-shifting “cash-box” outrage…

[T]he...

Brian Mustard, Sam Maruca, Charles Thériault, Richard Tremblay, "Transfer Pricing: What Are 'Reasonable Efforts,' and When should Penalties Apply?", Canadian Tax Foundation, 2015 Conference Report, 32:1-33

Alignment with OECD Guidelines (pp. 32:2-3)

[N]o Canadian legislation could explicitly refer to [the OECD] guidelines, nor indeed to any other...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(3) | 1526 | |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(4) - Paragraph 247(4)(a) | 102 |

Justice Marshall Rothstein, "An Overview of the Supreme Court of Canada", Bulletin for International Taxation (IBFD), January/February 2016, p. 20.

OECD guidelines (p. 24)

The OECD Guidelines do, however, have persuasive force in Canada. In Glaxo [2012 SCC 52], the provision of the Income Tax...

Derek G. Alty, Brian M. Studniberg, "The Corporate Capital Structure: Thin Capitalization and the ‘Recharacterization' Rules in Paragraphs 247(2)(b) and (d)", Canadian Tax Journal, (2014) 62:4, 1159-1202.

Dropping of explicit "recharacterization" reference and addition of non-tax purpose test to revised s. 247(2) (p. 1168)

In response to criticism...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 9 | 826 |

Ilana Ludwin, "Application of the Transactional Profit Split Method in Canada", Tax Management International Journal, 2015, p. 98.

Release of OECD Discussion Draft of TPSM (p. 98)

The Organisation for Economic Co-operation and Development (OECD) recently released its draft...

Mark D. Brender, Marc Richardson Arnould, Patrick Marley, "Cross-Border Cash-Pooling Arrangements Involving Canadian Subsidiaries: A Technical Minefield", Tax Management International Journal, 2014, p. 345.

Cash pooling description (p.345)

[W]e will examine a typical cash-pooling arrangement involving a Canadian subsidiary of a multinational group....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 17 - Subsection 17(7) | 268 |

J. Harold McClure, "Evaluating Whether a Distribution Affiliate Pays Arm's-Length Prices for Mining Products", Journal of International Taxation, July 2014, p. 33.

Development of Berry ratio (p. 37)

E.I. DuPont de Nemours & Co., 608 F.2d 445 (Ct. CL, 1979), was an influential transfer pricing case. As an...

Jules Lewy, Joel A. Nitikman, "Important Developments in Canadian Transfer Pricing", CCH Tax Topics, Number 2185, January 23, 2014, p. 1

Commissions charged by Elk to Japanese affiliate for securing logs (p.4)

Elk Trading [fn 5: Joel A. Nitikman was counsel for Elk.]

This appeal was...

Brian Bloom, François Vincent, "Canada's (Two) Transfer-Pricing Rules: A Tax Policy and Legal Analysis", 2011 CTF Conference Report, 20:1-40.

Objective of s. 247

20:3 The main objective in introducing new part XVI.1 [of the Act] was to enshrine the ALP [arm's length principle] in the...

Robert Couzin, "Policy Forum: The End of Transfer Pricing?", Canadian Tax Journal, (2013) 61:1, 159-78, at 172: He compares the approach to recharacterization in s. 247 of the Act and by the OECD:

[There is] the occasional need to "recharacterize" a transaction, as is permitted under the OECD guidelines where the transaction differs from...

Robert Feinschreiber, Margaret Kent, "OECD Transfer Pricing Guidelines and the 'Highly Uncertain' Valuation of Intangibles", Journal of International Taxation, February 2012, p. 47

Includes in Exhibit 2 a list of transfer pricing issues for the pharmaceutical industry which the OECD should address.

Richard G. Tremblay, "Canadian Transfer Pricing - The Arm's-Length Principle - Filling in the Blanks - Does an Arm's Length Price Ever Differ From Fair Market Value?", Tax Management International Journal, 2011, p. 599

The answer is "yes."

Johan Mayles, "CRA to Adopt OECD's Revised Transfer Pricing Guidelines", CCH Tax Topics, No. 2036, 17 March 2011, p.1

Review of comments of Jennifer Ryan, Director of International Tax division of the CRA at 24 February 2011 OBA section meeting - "CRA adheres to...

Danny Oosterhoff, Bo Wingerter, "The New OECD Guidelines: The Good, the Bad and the Ugly", International Transfer Pricing Journal, Vol. 18, No. 2, March/April 2011, p. 103.

Janice McCart, "Repatriation in Lieu of Secondary Adjustments", International Transfer Pricing Journal, Vol. 17, No. 1, January/February 2010, p. 65

Giammarco, Cottani, "OAC Discussion Draft on Transfer Pricing Aspects of Business Restructurings", Summary of Business Comments and Issues for Discussion", International Transfer Pricing Journal, Vol. 16, No. 4, 2009, p. 231.

Jennifer Rhee, "Unmasking 'Management Fees' - What's in a Name?", CCH Tax Topics, No. 1897, July 17, 2008, p. 1.

Brian Bloom, "Paragraph 247(2)(b) Demystified", CCH Tax Topics, 11 May 2006, No. 1783, p. 1.

Muris Dujsic, Matthew Billings, "Establishing Interest Rates in Intercompany Contacts", International Transfer Pricing Journal, Vol. 11, No. 6, November/December 2004, p. 247.

Todd Miller, Ryan Morris, "Canadian Subsidiary Guarantees for Foreign Parent Borrowings", Tax Notes International Vol. 34, No. 1, 5 April 2004, p. 63.

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 212 - Subsection 212(2) | 0 |

Bruce Sinclair, Robert Kopstein, "Guaranteed to Enlighten: The Impact of Guarantees on Financing Arrangements", 2000 Conference Report, c. 22.

Richard G. Tremblay, James Fuller, "Tax Consequences of Cross-Border Guarantee Fees", International Tax Planning, Vol. X, No. 3, 2001, p. 716.

Ivan Williams, "Contract Manufacturing Strategies: Tax-Saving Options for Intercompany Profit Allocation", Tax Topics, 21 March 2002, No. 1567, p. 1.

Robert Turner, "Cost Contribution Agreements", International Transfer Pricing Journal, 2001 Vol. 8, No. 3, p. 89.

Robert Turr, "Practical Application of Transactional Profit Methods", International Transfer Pricing Journal, Vol. 7, No. 5, September/October 2000, p. 184.

Jack Bernstein, "Transfer Pricing in Canada", Bulletin for International Fiscal Documentation, Vol. 53, No. 12, 1999, p. 570.

Janice McCart, Emma Purday, "What's The Deal? - Canada's New Rules on Arm's Length Pricing and Bundled Transactions", Tax Management International Journal, Vol. 28, No. 10, 8 October 1999, p. 633.

F. Vincent, I.M. Freedman, "Transfer Pricing in Canada: The Arm's Length Principle and the New Rules", 1997 Canadian Tax Journal, Vol. 45, No. 6, p. 1213.

Tipping, "British Bankers Comment on OECD's Draft on Global Trading of Financial Instruments", Tax Notes International, Vol. 15, No. 14, 6 October 1997, p. 1119.

Paragraph 247(2)(a)

See Also

Ingredion Canada Corporation v. The King, 2026 TCC 3

The Minister viewed the subject “hybrid instrument” cross-border intercompany transactions as something that should be recharacterized as an...

Singapore Telecom Australia Investments Pty Ltd v Commissioner of Taxation, [2021] FCA 1597, aff'd [2024] FCAFC 29

In June 2002, a Singapore-resident company (“SAI”) transferred the shares of a recently-acquired Australian telecom company (“SOPL”) to an...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 9 | loan with interest that would vary significantly depending on whether cash flow conditions were met would not have been agreed to by independent enterprises | 524 |

Commissioner of Taxation v Glencore Investment Pty Ltd, [2020] FCAFC 187

An Australian subsidiary (“CMPL”) of Glencore Switzerland (“GIAG”), which had a high-cost copper mine, agreed with GIAG (who was the sole...

Agracity Ltd. v. The Queen, 2020 TCC 91

A Barbados international business corporation (“NewAgco Barbados”), that was a subsidiary of a Canadian company owned by two Canadian...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Sham | confused books and records, where no intent to deceive, were not indicative of sham | 574 |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) - Paragraph 247(2)(b) | no evidence proffered that arm’s length parties would not have entered into non-resident goods seller/domestic servicing transactions | 494 |

| Tax Topics - General Concepts - Onus | Hickman Motors followed, but same result under Sarmadi | 331 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a.1) | assessments based on s. 95(2)(a)(a.1) dropped by Crown | 221 |

Burlington Resources Finance Company v. The Queen, 2020 TCC 32

Burlington, a Nova Scotia ULC, borrowed approximately U.S.$3 billion in 2001 and 2002 by issuing notes that were guaranteed by its non-resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Federal - Tax Court of Canada Rules (General Procedure) - Section 132 | in context, no formal admission made - and any admission could be withdrawn in the interests of justice | 555 |

| Tax Topics - Other Legislation/Constitution - Federal - Tax Court of Canada Rules (General Procedure) - Section 54 | amendment permitted in advance of trial to give effect to previously disclosed Crown position | 307 |

Glencore Investment Pty Ltd v Commissioner of Taxation of the Commonwealth of Australia, [2019] FCA 1432, largely aff'd [2020] FCAFC 187

The taxpayer was assessed as the head of a multiple entry consolidated group for Australian tax purposes, of which Cobar Management Pty Ltd...

Administrative Policy

5 May 2021 IFA Roundtable Q. 7, 2021-0887521C6 - Section 247, FAPI & Subsection 80.4(2)

A wholly-owned foreign subsidiary (FS) of CanCo uses funds generated from its operations to make a non-interest bearing loan to a foreign borrower...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(3) - Paragraph 214(3)(a) | non-interest-bearing loan from a CFA to a NR sister of the Canadian taxpayer generates a deemed dividend to the sister under ss. 80.4(2) and 214(3)(a) – plus FAPI to CFA | 348 |

| Tax Topics - Income Tax Act - Section 80.4 - Subsection 80.4(2) | a non-interest-bearing loan from a CFA to a NR sister of the Canadian taxpayer generated double tax (FAPI and Pt. XIII tax) | 218 |

5 May 2021 IFA Roundtable Q. 4, 2021-0887601C6 - 2021 IFA Q4 - section 247 Post Cameco

Regarding the CRA response to the TCC and FCA decisions in Cameco, CRA stated “that these decisions may limit situations where the...

7 October 2020 APFF Roundtable Q. 10, 2020-0852221C6 F - Interest-free loan to a related foreign company

Is an individual who makes an interest-free loan to a non-resident corporation with which the individual does not deal at arm's length required to...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 17 - Subsection 17(1.1) | s. 17 generally does not apply to loans made by individuals, but s. 247 can apply | 121 |

3 February 2021 Transfer Pricing Webinar of the Canadian Tax Foundation: Panel IV: Selected Topics in Transfer Pricing

Application of s. 247(2) to transactions between non-residents

- Regarding the finding in 2017-0691191C6 that the transfer pricing rules can apply...

3 February 2021 Transfer Pricing Webinar of the Canadian Tax Foundation: Panel I: Transfer Pricing Audits and Competent Authority

TPM-17 maintained re CEWS subsidies

- Notwithstanding somewhat different views of the OECD, CRA will continue to evaluate transfer prices in...

15 September 2020 IFA Roundtable Q. 5, 2020-0853401C6 - IFA 2020 Q5: TPM-17 and COVID-19

TPM-17 provides that the cost base should not be reduced by government assistance unless there is reliable evidence that arm’s length parties...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 9 | Cdn governmental COVID assistance generally does not reduce cost | 138 |

2020 IFA-YIN Seminar on COVID-19 Guidelines, Q.12

What is the impact and treatment of the COVID-19 related government assistance programs in the context of TPM-17?

CRA indicated that such position...

Articles

Nakul Kohli, "Sharing COVID-19 Assistance with Foreign Entities Through Transfer Pricing", COVID-19 and Canadian Tax for the Owner-Manager/Canadian Tax Focus (Canadian Tax Foundation), July 2020, p. 5

TPM-17 policy (p.4)

…TPM-17 ... states that when a Canadian taxpayer receives government assistance and participates in a cross-border...

Paragraph 247(2)(b)

Cases

Canada v. CAMECO Corporation, 2020 FCA 112

In 1999, the Luxembourg subsidiary (“CESA”) of the taxpayer (“Cameco”) entered into a long-term contract (the “HEU Feed Agreement”)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Marginal Notes | marginal note referred to as indication of provision’s thrust | 68 |

See Also

BlackRock HoldCo 5, LLC v Commissioners for His Majesty's Revenue and Customs, [2024] EWCA Civ 330

The structure for the acquisition by the BlackRock group of the U.S. target (“BGI”) entailed a BlackRock LLC (“LLC4”) lending US$4...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 9 | to make a cross-border inter-affiliate loan comparable in risk to the hypothetical independent enterprises’ loan, risk-protection covenants were to be imputed to the latter | 480 |

Revenue and Customs v Blackrock Holdco 5 LLC, [2022] UKUT 199 (TCC), overruled on transfer-pricing analysis but aff'd on other grounds at [2024] EWCA Civ 330

The structure for the acquisition by the BlackRock group of the North American management business of Barclays Global Investors (“BGI”)...

Agracity Ltd. v. The Queen, 2020 TCC 91

The taxpayer (“AgraCity”) was a resident corporation wholly-owned by a resident individual (James Mann) that between 2005 and 2008 promoted...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Sham | confused books and records, where no intent to deceive, were not indicative of sham | 574 |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) - Paragraph 247(2)(a) | fee earned by Canadian servicer fell within “rough, but … acceptable, range of what an arm’s length service provider might have enjoyed” | 303 |

| Tax Topics - General Concepts - Onus | Hickman Motors followed, but same result under Sarmadi | 331 |

| Tax Topics - Income Tax Act - Section 95 - Subsection 95(2) - Paragraph 95(2)(a.1) | assessments based on s. 95(2)(a)(a.1) dropped by Crown | 221 |

Administrative Policy

15 September 2020 IFA Roundtable Q. 3, 2020-0853371C6 - IFA 2020 Q3: Draft IC71-17R6, Paragraph 43

Please elaborate on the statement in draft IC71- 17R5, para. 43, that s.247(2)(b) is one of the Act’s “anti-avoidance provisions.” Where...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 26 | Canada does not negotiate away its application of domestic anti-avoidance rules | 84 |

2020 IFA-YIN Seminar on COVID-19 Guidelines, Q. 17

Given the recent FCA decision in Cameco (and assuming that it is a final decision), does CRA foresee modifying assessing practices relative to...

Paragraph 247(2)(d)

Administrative Policy

3 February 2021 Transfer Pricing Webinar of the Canadian Tax Foundation: Panel IV: Selected Topics in Transfer Pricing

OECD “delineation” of thin cap loan is likely partial recharacterization, which is acceptable

- Paragraph 10.13 of BEPS chapter 10 references a...

3 February 2021 Transfer Pricing Webinar of the Canadian Tax Foundation: Panel I: Transfer Pricing Audits and Competent Authority

S. 247(2)(d) no longer a tool of last resort

- CRA cancelled IC 87-2R “International Transfer Pricing” as it was misleading regarding...

CRA Notice to tax professionals 5 July 2019

Hybrid mismatch arrangements are tax plans intended to secure a tax advantage within a multinational enterprise by exploiting differences in the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(3) | CRA successfully applied transfer pricing penalties to an inbound hybrid loan | 258 |

27 March 2019 CTF Seminar - Transfer Pricing

In practice, where CRA concludes that there should be recharacterizion under ss. 247(2)(b) and (d), it considers itself to be implicitly finding...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(10) | downward-adjustment requests reviewed for whether there is double non-taxation | 115 |

| Tax Topics - Income Tax Act - Section 233.8 - Subsection 233.8(3) | use of CbC reports for assessing risk | 41 |

| Tax Topics - Income Tax Act - Section 231.1 - Subsection 231.1(1) - Paragraph 231.1(1)(a) | access to tax accrual working papers only where necessary | 110 |

Subsection 247(2.03)

Articles

Michael Kandev, "Interpretation or Delegation: The Increasing Prevalence of Formal References to OECD Materials", International Tax Highlights, Vol. 2, No. 3, August 2023, p. 9

ITA rules referencing potentially ambulatory OECD guidelines (pp. 9-10)

- ITA s. 270(2) specifies that the provisions in Pt. XIX are to be...

Subsection 247(2.1)

Administrative Policy

6 September 2023 Internal T.I. 2019-0805481I7 - Interaction of 17.1(1) & 247(2)

A non-resident corporation (Parent2) which, through a wholly-owned non-resident subsidiary, was the sole shareholder of a corporation resident in...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 17.1 - Subsection 17.1(1) | interest can be imputed under s. 247(2) to a PLOI which already is subject to s. 17.1 imputed interest | 240 |

3 February 2021 Transfer Pricing Webinar of the Canadian Tax Foundation: Panel IV: Selected Topics in Transfer Pricing

S. 247(2.1) ordering rule is clarifying

- S. 247(2.1) effected clarifying amendments. Admittedly, the CRA might have considered the proposed...

Finance

15 May 2019 IFA Finance Roundtable – “Proposed s. 247(1.1)”

The purpose of s. 247(1.1) was to resolve ambiguity as to the ordering of the respective operations of Parts I and XVI.1 – for example, where a...

Articles

Nathan Boidman, Michael N. Kandev, "Evaluating Canada’s Attempt to Reconcile General Transfer Pricing Rules and Specific Antiabuse Provisions", Tax Notes International Vol. 98, No. 6, May 11, 2020, p. 699

Failure of Finance Notes to reflect that s. 247(2.1) begins with “initial amounts” that already reflect other ITA provisions’ application...

Marc Roy, "Proposed Transfer Pricing Ordering Rules", International Tax (Wolters Kluwer CCH), December 2019, No. 109, p. 3

Intent in Explanatory Notes to apply s. 247(2) 1st (pp. 5-6)

It is clear from the examples in the technical notes that the intent would be to...

François Fournier-Gendron, "Amendments to the Act: The Impact of Proposed Subsection 247(2.1) on Section 17", Canadian Tax Highlights, Vol. 27, No. 12, December 2019, p. 5

Potential imputation of interest under s. 247(2.1) irrespective of the operation of s. 17 (p. 5)

Subsection 247(2.1) will … affect the...

Joint Committee, "Transfer Pricing Amendments", 5 November 2019 Joint Committee letter

The draft legislation, whose general premise that s. 247(2) applies in priority to all other provisions of the Act, creates ambiguity as to the...

Joint Committee, "Foreign Affiliate Dumping, Derivative Forward Agreement and Transfer Pricing Amendments Announced in the 2019 Federal Budget", 24 May 2019 Submission of the Joint Committee

- S. 247(1.1) is circular.

Subsection 247(3)

Administrative Policy

27 February 2024 CTF Transfer Pricing Roundtable

In its supporting documentation the taxpayer should not simply state that agreements with third parties were reviewed and none were...

| Other locations for this summary | |

|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(3) |

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | 506 | |

| Tax Topics - Income Tax Act - Section 231.1 - Subsection 231.1(1) | 159 | |

| Tax Topics - Income Tax Act - Section 271 - Subsection 271(4) | 74 |

3 February 2021 Transfer Pricing Webinar of the Canadian Tax Foundation: Panel I: Transfer Pricing Audits and Competent Authority

Meaning of TPRC insufficient documentation notation

- The Transfer Pricing Review Committee typically indicates that “the documentation provided...

CRA Notice to tax professionals 5 July 2019

CRA provided a cryptic diagram portraying a borrowing by Canco of, say, $100M from U.S. parent (a C Corp) at, say, 10% interest, with Canco...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) - Paragraph 247(2)(d) | s. 247(2)(d) applied to inbound hybrid loan | 277 |

14 September 2016 Internal T.I. 2016-0631631I7 - Transfer pricing capital adjustment

In Year X , Canco buys a non-depreciable capital property from its non-resident parent (Forco) for $10,000,000, sells the property for $15,000,000...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | s. 247(2) ACB adjustment can be made in statute-barred year | 277 |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(11) | s. 152(4) limits apply to additional s. 247(3) assessments | 161 |

TPM-09 Reasonable efforts under section 247 of the Income Tax Act, September 18, 2006

- When preparing documentation the taxpayer should attempt to weigh the significance of the transactions in relation to their business with the...

Articles

Brian Mustard, Sam Maruca, Charles Thériault, Richard Tremblay, "Transfer Pricing: What Are 'Reasonable Efforts,' and When should Penalties Apply?", Canadian Tax Foundation, 2015 Conference Report, 32:1-33

Unlikelihood of a s. 247(4)(a) safe harbour (p. 32:7)

[T]he qualitative assessment of the adequacy of the actions described in subsection 247(4)...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | 110 | |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(4) - Paragraph 247(4)(a) | 102 |

Michael Colborne, Michael McLaren, Mark Barbour, "Subsection 247(3): What are "Reasonable Efforts"?", Canadian Tax Journal, (2016) 64:1, 229-43

Dictionary meaning of “reasonable efforts” (p. 236)

On the basis of these definitions, we believe that the ordinary meaning of "reasonable...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(4) | 101 |

Paragraph 247(3)(a)

Subparagraph 247(3)(a)(iii)

Administrative Policy

10 October 2014 APFF Roundtable Q. 26, 2014-0538201C6 F - 2014 APFF Roundtable, Q. 26 - Cost of property

After responding to a question on the interrelationship between ss. 69 and 247 respecting a cross-border non-arm's length purchase by a Canadian...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Fair Market Value - Shares | definition of FMV, which may differ from the s. 247 arm's length price | 182 |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | arm's length transfer price prevails over FMV | 182 |

Paragraph 247(3)(b)

Subparagraph 247(3)(b)(ii)

Administrative Policy

5 May 2021 IFA Roundtable Q. 3, 2021-0888281C6 - IFA 2021 Q.3: 247(3) - C$5 M Threshold & 261(5)

A Canadian corporation (“Canco”) with an elected functional currency is subject to transfer pricing income adjustments respecting a functional...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 261 - Subsection 261(5) - Paragraph 261(5)(b) | the C$5M threshold in s. 247(3)(b)(ii) is to be translated into a functional currency on the basis that it is not “in respect of a penalty” | 282 |

Subsection 247(4)

See Also

Marzen Artistic Aluminum Ltd. v. The Queen, 2014 DTC 1145 [at at 3433], 2014 TCC 194, aff'd 2016 DTC 5018 [at 6600], 2016 FCA 34

"Marketing fees" paid by taxpayer to its Barbados subsidiary were found to be well in excess of the arm's length amount mandated by s. 247(2). ...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | separate entity approach endorsed | 521 |

McKesson Canada Corporation v. The Queen, 2014 DTC 1040 [at at 2723], 2013 TCC 404

FCA appeal settled.

The only documentary support for the discount at which the taxpayer sold receivables to its Luxembourg parent (which Boyle J...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - General Concepts - Evidence | expert reports without testimony | 56 |

| Tax Topics - General Concepts - Purpose/Intention | tax purpose v. commercial result | 92 |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | terms adjusted within framework of transaction chosen by taxpayer | 928 |

| Tax Topics - Treaties - Income Tax Conventions - Article 9 | 5-year limitation did not apply to secondary Part XIII assessment | 206 |

Administrative Policy

17 May 2022 IFA Roundtable Q. 9, 2022-0926341C6 - Contemporaneous Docs and COVID-19

Will CRA provide any COVID-related relief regarding the requirement under s. 247(4) to complete contemporaneous documentation (“CD”) meeting...

16 May 2018 IFA Roundtable Q. 4, 2018-0748171C6 - Penalties for Non-Residents

CRA indicated that it will not provide any special safe harbour for a non-resident corporation that did not make any T2 filings (other than a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 220 - Subsection 220(3) | a non-resident who incorrectly claimed a no-PE Treaty exemption can apply for penalty relief | 129 |

29 November 2016 CTF Roundtable Q. 9, 2016-0669801C6 - BEPS Action Item 13

Does CRA expect that the “reasonable efforts” that a taxpayer must make to determine and use arm’s length transfer prices include the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 233.8 - Subsection 233.8(3) | no requirement to produce a Local or Master File | 77 |

TPM-05R – Requests for Contemporaneous Documentation 28 March 2014

9. [issuance of requests] Requests for contemporaneous documentation must be issued at the stage of initial contact with the taxpayer in all...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Statutory Interpretation - Interpretation Act - Section 26 | 50 | |

| Tax Topics - Statutory Interpretation - Interpretation Act - Section 28 | 109 |

Articles

Michael Colborne, Michael McLaren, Mark Barbour, "Subsection 247(3): What are "Reasonable Efforts"?", Canadian Tax Journal, (2016) 64:1, 229-43

Standalone report not required/may be no assumptions and policies (p. 232)

[T]he statute does not require that the taxpayer condense all of the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(3) | 490 |

Martin Przysuski, Srini Lalapet, "Appropriate Canadian Transfer Pricing Documentation", Tax Notes International, 3 October 2005, p. 55.

Paragraph 247(4)(a)

Administrative Policy

26 February 2019 Toronto CRA & Tax Professionals Seminar

CRA stated:

- Penalties are usually imposed for failure to have accurate and complete contemporaneous documentation respecting the ss....

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | BEPS has not substantially affected CRA's transfer-pricing practices | 178 |

Articles

Brian Mustard, Sam Maruca, Charles Thériault, Richard Tremblay, "Transfer Pricing: What Are 'Reasonable Efforts,' and When should Penalties Apply?", Canadian Tax Foundation, 2015 Conference Report, 32:1-33

Minor subsequent corrections (p. 32:8)

[I]t may, of course, happen that a transfer-pricing report is substantially completed by the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | 110 | |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(3) | 1526 |

Subsection 247(7)

Administrative Policy

5 May 2021 IFA Roundtable Q. 5, 2021-0887671C6 - 2021 IFA Q5 - Applicability of 247(7)

A limited partnership (LP) between two resident related corporations (ACo and BCo) made a non-interest bearing loan to FA, which was wholly-owned...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 17 - Subsection 17(8) | s. 17(18) exclusion for loan by related Cdn. parternship to LP did not apply for s. 247(7) purposes | 191 |

26 April 2017 IFA Roundtable Q. 1, 2017-0691071C6 - Interaction between s17 and s247

(a) A non-interest bearing loan made by a corporation resident in Canada to a wholly-owned non-resident subsidiary remains outstanding for...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 17 - Subsection 17(1.1) | s. 17(1) does not oust application of s. 247(2) | 89 |

Articles

Brian Bloom, "A Policy of Disengagement: How Subsection 247(2) Relates to the Act's Income- Modifying Rules", CCH Tax Topics, No. 1957, 10 September 2009, p. 1.

Subsection 247(7.1)

Administrative Policy

31 March 2014 External T.I. 2013-0515661E5 - Subsection 247(7.1) coming into-force rule

The election [in the coming-into-force provision] is intended to provide a taxpayer the benefit of an exception to the transfer price adjustment...

Articles

Geoffrey S. Turner, "Downstream Loan Guarantees and Subsection 247(7.1) Transfer Pricing Relief", CCH Tax Topics, No. 2166, September 12, 2013, p.1:

Narrowness of (active business) requirement of s. 247(5.1) (p. 2)

The proposed subsection 247(7.1) relief from transfer pricing requirements will,...

Subsection 247(8)

Administrative Policy

19 December 2013 Internal T.I. 2013-0490751I7 - Adjustment to a taxpayer`s CDA

The taxpayer, which was a private corporation, disposed of eligible capital property to a non-arm's-length non-resident sister company...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 89 - Subsection 89(1) - Capital Dividend Account | s. 247(2) increase to ecp proceeds increased CDA on transaction effective date | 87 |

Subsection 247(10)

Cases

Meglobal Canada Ulc v. Canada, 2026 FCA 24

In objections of the taxpayer (MEGlobal) to reassessments of three of its taxation years to reflect upward transfer pricing adjustments under s....

Dow Chemical Canada ULC v. Canada, 2024 SCC 23

The Minister indicated that she would not exercise her discretion to allow the request of the Canadian taxpayer (“Dow”) a requested...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 171 - Subsection 171(1) - Paragraph 171(1)(b) - Subparagraph 171(1)(b)(iii) | Tax Court lacks jurisdiction to vary or quash an s. 247(10) opinion of the Minister | 128 |

| Tax Topics - Income Tax Act - Section 152 - Subsection 152(1) | assessment is a product and does not reference the process in arriving at it | 43 |

Canada v. Dow Chemical Canada ULC, 2022 FCA 70, leave granted 23 February 2023

The Minister reassessed the 2006 taxation year of the (Canadian-resident) taxpayer (“Dow”) by adding 307 million in a transfer-pricing...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Federal - Federal Courts Act - Section 18.5 | Ministerial decision to deny a s. 247(10) downward adjustment cannot be appealed under s. 247(11) and, therefore, is not rendered non-reviewable by s. 18.5 | 259 |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(11) | Ministerial decision to deny a s. 247(10) downward adjustment cannot be appealed under s. 247(11) | 176 |

| Tax Topics - Income Tax Act - Section 171 - Subsection 171(1) | Tax Court cannot reverse a CRA opinion that a requested s. 247(10) downward adjustment is inappropriate | 277 |

| Tax Topics - Income Tax Act - Section 169 - Subsection 169(1) | an appeal of an assessment is of an amount, not of an opinion leading to the assessment | 157 |

See Also

MEGLobal Canada ULC v. The King, 2025 TCC 50, aff'd 2026 FCA 24

In objections of the taxpayer to the Minister’s reassessments of its 2008, 2010 and 2011 taxation years to reflect upward transfer pricing...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 171 - Subsection 171(1) - Paragraph 171(1)(b) - Subparagraph 171(1)(b)(iii) | s. 171(1)(b)(iii) did not authorize the Tax Court providing an opinion that the taxpayer’s requested downward adjustment accorded with a proper s. 247(2) analysis | 242 |

Dow Chemical Canada ULC v. The Queen, 2020 TCC 139, rev'd 2022 FCA 70

Following the resolution of transfer pricing adjustment issues addressed by the Canadian and Swiss competent authorities respecting the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(11) | s. 247(11) only addresses penalty assessments | 197 |

| Tax Topics - Income Tax Act - Section 171 - Subsection 171(1) | the range of s. 171 remedies can be applied to an assessment that does not implement a requested s. 247(10) downward adjustment | 365 |

Administrative Policy

Memorandum TPM-03 "Downward Transfer Pricing Adjustments, 21 June 2022

Where downward adjustments are acceptable

8. Downward transfer pricing adjustments are not intended to serve as a vehicle for taxpayers to...

3 February 2021 Transfer Pricing Webinar of the Canadian Tax Foundation: Panel I: Transfer Pricing Audits and Competent Authority

Downward adjustments generally not granted if double non-taxation results

- The general concept animating CRA’s approach to determining whether...

27 March 2019 CTF Seminar - Transfer Pricing

S. 247(10) states that a downward adjustment shall not be made unless it is “appropriate in the circumstances.” How is this discretion...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) - Paragraph 247(2)(d) | 3-step process before s. 247(2)(d) is applied | 175 |

| Tax Topics - Income Tax Act - Section 233.8 - Subsection 233.8(3) | use of CbC reports for assessing risk | 41 |

| Tax Topics - Income Tax Act - Section 231.1 - Subsection 231.1(1) - Paragraph 231.1(1)(a) | access to tax accrual working papers only where necessary | 110 |

Update - Competent Authority Services Division, 20 December 2013

Where a Canadian entity requests a reduction of its Canadian taxable income (downward transfer pricing adjustment) where the request relates to a...

Memorandum TPM-03 "Downward Transfer Pricing Adjustments Under Subsection 247(2)," 20 October 2003

When s. 247(10) discretion exercised

The Minister may decide not to exercise discretion under s. 247(10) where a Canadian company requests a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 15 - Subsection 15(1) | 100 |

Articles

Daniel Sandler, Lisa Watzinger, "Disputing Denied Downward Transfer-Pricing Adjustments", Canadian Tax Journal, (2019) 67:2, 281-308

Appeals Branch will not review s. 247(10) downward adjustments (p. 287)

[N]o one in CRA Appeals has delegated authority under subsection 247(10),...

| Other locations for this summary | |

|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(10) |

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(11) | 940 |

Nathan Boidman, "Canadian Approach to Downward Pricing Adjustments: CCRA's 18 March 2003 Communiqué", International Transfer Pricing Journal, Vol. 10, No. 5 2003, p. 181.

Subsection 247(11)

Cases

Canada v. Dow Chemical Canada ULC, 2022 FCA 70, leave granted 23 February 2023

The Minister reassessed the 2006 taxation year of the (Canadian-resident) taxpayer (“Dow”) by adding 307 million in a transfer-pricing...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Other Legislation/Constitution - Federal - Federal Courts Act - Section 18.5 | Ministerial decision to deny a s. 247(10) downward adjustment cannot be appealed under s. 247(11) and, therefore, is not rendered non-reviewable by s. 18.5 | 259 |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(10) | Tax Court cannot review a s. 247(10) downward adjustment because it only has the ITA s. 171 jurisdiction to deal with an assessment and not with a s. 247(10) opinion | 354 |

| Tax Topics - Income Tax Act - Section 171 - Subsection 171(1) | Tax Court cannot reverse a CRA opinion that a requested s. 247(10) downward adjustment is inappropriate | 277 |

| Tax Topics - Income Tax Act - Section 169 - Subsection 169(1) | an appeal of an assessment is of an amount, not of an opinion leading to the assessment | 157 |

See Also

Dow Chemical Canada ULC v. The Queen, 2020 TCC 139, rev'd 2022 FCA 70

In reassessing the taxpayer under s. 247(2), the Minister did not allow a requested “downward” adjustment under s. 247(10) (to increase the...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(10) | TCC has jurisdiction to review whether a CRA denial of a downward s. 247(10) adjustment was “correct in fact and law" | 806 |

| Tax Topics - Income Tax Act - Section 171 - Subsection 171(1) | the range of s. 171 remedies can be applied to an assessment that does not implement a requested s. 247(10) downward adjustment | 365 |

Administrative Policy

14 September 2016 Internal T.I. 2016-0631631I7 - Transfer pricing capital adjustment

In the situation where Canco acquired a non-depreciable capital property in Year X from an affiliate at a price that was substantially in excess...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(2) | s. 247(2) ACB adjustment can be made in statute-barred year | 277 |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(3) | no statute-barring applies to initial assessments of transfer-pricing penalties | 326 |

Articles

Daniel Sandler, Lisa Watzinger, "Disputing Denied Downward Transfer-Pricing Adjustments", Canadian Tax Journal, (2019) 67:2, 281-308

Quaere whether s. 247(11) accords the TCC jurisdiction to hear an appeal of a s. 247(10) downward adjustment (p. 288)

[I]f subsection 247(10) is...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(10) | 219 | |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(10) |

Subsection 247(12)

Administrative Policy

18 April 2019 Internal T.I. 2018-0753621I7 - Subsection 247(12)

CRA proposed an inclusion in Canco’s income under s. 247(2) of the difference between an arm’s length price for goods sold by Canco to a...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Treaties - Income Tax Conventions - Article 10 | secondary adjustment benefit to a NR sister was a dividend for Treaty purposes | 221 |

| Tax Topics - Treaties - Income Tax Conventions - Article 4 | a s. 247(12) secondary-adjustment deemed dividend paid by Canco to an LLC sister qualified under Art. IV(6) for the 5% Treaty-reduced rate on dividends to its U.S. parent | 498 |

19 November 2014 Internal T.I. 2014-0530911I7 F - Transfer pricing secondary adjustments

An expense is incurred by a non-resident corporation, which carries on business in Canada through a permanent establishment, and paid to a...

TPM-02R Secondary Transfer Pricing Adjustments, Repatriation and Part XIII Tax Assessments 1 June 2021

Scope of secondary adjustments

- Where a taxpayer (including for TPM-02R purposes, a partnership) is subject to a “primary adjustment” under...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(3.1) | 89 | |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(13) | 605 | |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(14) | 104 | |

| Tax Topics - Income Tax Act - Section 227 - Subsection 227(8.5) - Paragraph 227(8.5)(b) | no penalty re secondary adjustments even if not pursuant to s. 247(12) | 99 |

| Tax Topics - Income Tax Act - Section 227 - Subsection 227(8) | no penalty re secondary adjustments even if no repatriation agreement | 99 |

Articles

Joel A. Nitikman, "Section 247 – Secondary Adjustments, Deemed Dividends, Repatriation and Interest", International Tax Planning (Federated Press), Vol. XVIII, No.1, 2012, p. 1224, at p.1225

Where Canco pays an excessive amount to a Forper [namely, a particular non-resident person] that is a non-resident sister corporation in the same...

Subsection 247(13)

Administrative Policy

TPM-02R Secondary Transfer Pricing Adjustments, Repatriation and Part XIII Tax Assessments 1 June 2021

Requirements of CRA repatriation policy

- CRA will apply the following administrative repatriation policy to all taxpayers (not only those to whom...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(12) | 439 | |

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(3.1) | 89 | |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(14) | 104 | |

| Tax Topics - Income Tax Act - Section 227 - Subsection 227(8.5) - Paragraph 227(8.5)(b) | no penalty re secondary adjustments even if not pursuant to s. 247(12) | 99 |

| Tax Topics - Income Tax Act - Section 227 - Subsection 227(8) | no penalty re secondary adjustments even if no repatriation agreement | 99 |

Articles

Joel A. Nitikman, "Section 247 – Secondary Adjustments, Deemed Dividends, Repatriation and Interest", International Tax Planning, Vol. XVIII, No.1, 2012, p. 1224, at p. 1226:

It is not clear why the reduction is only for the amount that the Minister considers appropriate....The Joint Committee recommended that the...

Subsection 247(14)

Administrative Policy

TPM-02R Secondary Transfer Pricing Adjustments, Repatriation and Part XIII Tax Assessments 1 June 2021

Interest not applied if repatriation agreement accepted

35. Subsection 247(14) of the ITA provides that if the non-arm’s length non-resident...

| Locations of other summaries | Wordcount | |

|---|---|---|

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(12) | 439 | |

| Tax Topics - Income Tax Act - Section 214 - Subsection 214(3.1) | 89 | |

| Tax Topics - Income Tax Act - Section 247 - New - Subsection 247(13) | 605 | |

| Tax Topics - Income Tax Act - Section 227 - Subsection 227(8.5) - Paragraph 227(8.5)(b) | no penalty re secondary adjustments even if not pursuant to s. 247(12) | 99 |

| Tax Topics - Income Tax Act - Section 227 - Subsection 227(8) | no penalty re secondary adjustments even if no repatriation agreement | 99 |